What digital body language can reveal about online customers

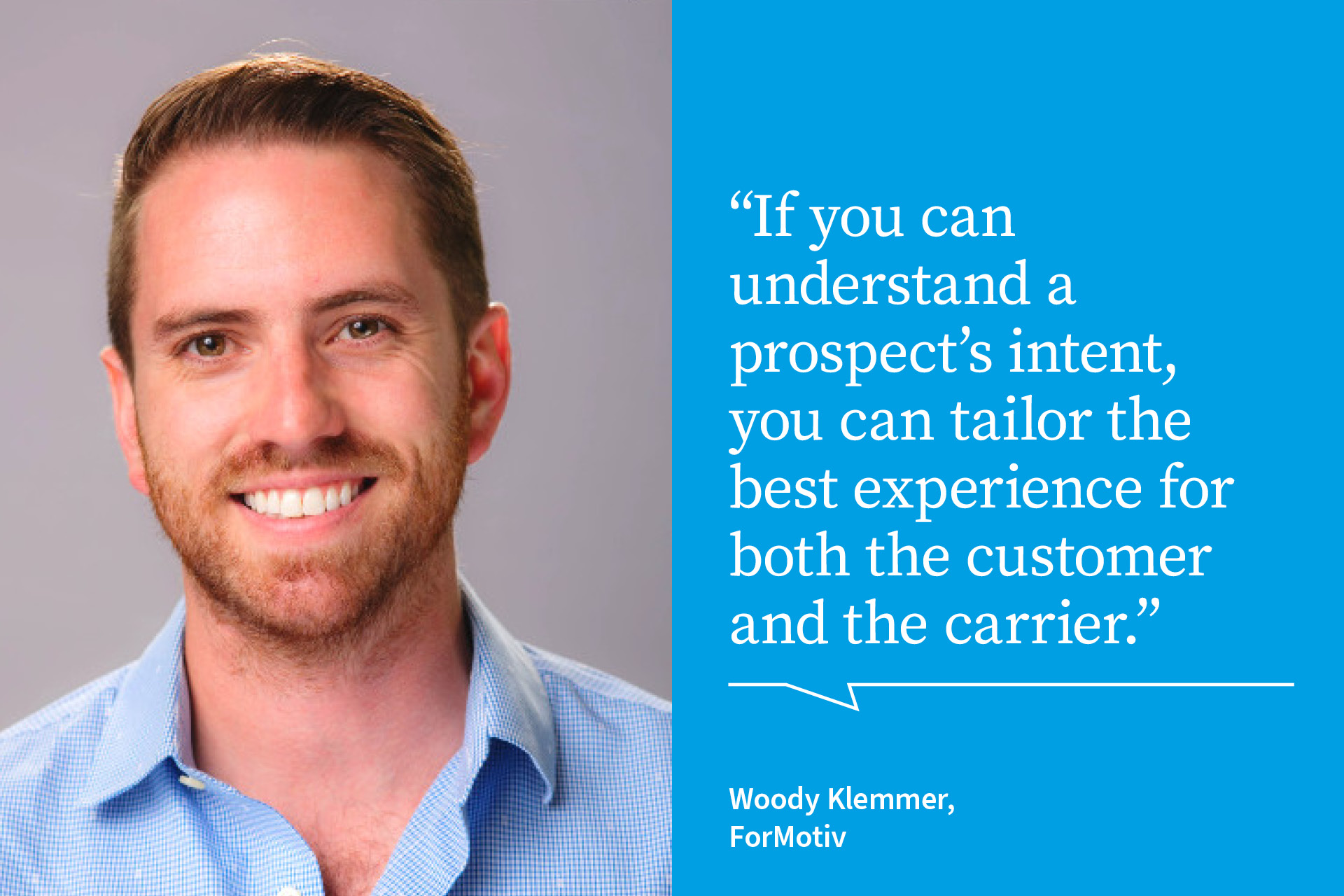

Behavioural data science can be used to understand the purchase intent and risk profile of digital applicants even while they are still filling out online applications – helping insurers improve onboarding efficiency and spot fraud, says Woody Klemmer, Head of Growth at ForMotiv, a US-based behavioural data science platform.

Behavioural data science, which combines behavioural analytics and real-time machine learning to understand how people behave, is increasingly being used by insurers to help them improve the way they interact with their customers, especially online.

Today it’s even possible to gain actionable insights from the way customers behave as they fill out an online application form.

“Similar to how body language, tone of voice, eye contact and other non-verbal cues are important in understanding someone’s intent in person, digital body language provides a similar level of insight during online insurance applications."

“Imagine a user filling out an online insurance quote who makes their way through the application, sees a quote, but doesn’t purchase. That user may simply be window shopping and would be a prime candidate for a real-time nudge, a phone call or outbound marketing effort,” he explains. “But what if another applicant provided the exact same responses, except this user was copying/pasting important personal information, typing inhumanly fast, then got to the quote page and abandoned it. That applicant could be a bot attempting to scrape pre-fill information to use for nefarious purposes, so you would likely want to treat that user differently. The issue is that carriers only see the final answer provided by the customer, but how they enter the information is equally if not more important than what they ultimately submit.”

Using a behavioural data science solution like ForMotiv, an insurer can triage any risky product submissions and send them for further evaluation.

Most carriers leverage ForMotiv’s solutions in real-time via API to drive the next best action for the applicant. The technology can be applied across the range of consumer insurances and ForMotiv currently works with several top ten property & casualty and life insurance companies.

Insurers using such applications might have different goals in mind. Those that are in growth mode would focus on conversion solutions that predict the purchase intent of applicants, enabling them to drive the next best action to close more business and/or create a better user experience.

Alternatively, when profitability is a priority, insurers might focus on leakage, non-disclosure and fraud solutions to improve their bottom line and identify risky or bad business.

But are there any constraints on using the technology, around bias, discrimination or exclusion risk? Klemmer thinks not: “We do not capture any personally identifiable information, and carriers do not use us to make underwriting pricing decisions. Instead, they use us to feel more confident about the applicants who are accelerated, while more accurately triaging applicants who require further review.”

The techniques pioneered by companies like ForMotiv will keep evolving in line with further advances in AI, and Klemmer believes that emerging Vertical SaaS companies can drive hyper-personalisation and better risk management, as well as deterring old and new kinds of fraud.

This will also result in faster and more accurate underwriting and claims processing. “We think this trend is a great tailwind for us, as more and more aspects of insurance go digital and require real-time triage decisions,” he predicts.

Kate Baldry, Underwriting Research & Systems Developer at the Hannover Re UK Life Branch, is a member of the group’s wider Behavioural Science unit. She’s been following developments closely.

“For the past decade, insurers have been considering behavioural science techniques to better understand customers’ actions. Why is a customer doing what they are doing? For example, are they hesitating when they complete a question on the application form because they are recalling information; deciding how to answer it; is the question too complicated; or is it something else?” Baldry says. Gathering these types of insight means that the insurer can continuously improve their processes to ensure the smoothest journey for the customer.

“As we know, customers are not one homogenous group, so it’s important to recognise this and create appropriate solutions where possible,” Baldry concludes.

ForMotiv provides insurtech solutions that give carriers actionable insight into the purchase intent and potential risk of their digital applicants, all in real time. Philadelphia-based ForMotiv works with leading carriers including several top ten life and property & casualty clients, reinsurers, eApp providers, and more across the insurance space. ForMotiv was founded in 2018.

User questions

Answered questions

Unanswered questions

Views: 715

Downloads: 0

| 0 % | |

| 0 % | |

| 0 % | |

| 0 % | |

| 0 % |

Page is favored by 0 user.

Contact inquiries: 0